Airbnb’s AirCover Protection: An Honest Examination

The first thing to understand about Airbnb’s Aircover protection is that it does not replace a host’s current Homeowners insurance. It’s such an important fact, that it’s listed as the #3 FAQ on the AirCover protection landing page, as seen below.

Why is AirCover Recommending You Call Your Insurance Company?

If you do not fully disclose your Airbnb rental activity to your insurance provider, then they can virtually deny any insurance claim. There are plenty of well-documented lawsuits over the years, where Airbnb AirCover Protection would have made no difference. This is because the damage had nothing to do with the rental of the property, yet the insurance carrier still denied coverage.

There is a terrible misconception in the short-term rental industry that a property owner can simply purchase a standard homeowner’s policy and then rely on Airbnb’s Aircover to protect the property while it’s being rented. This couldn’t be further from the truth. Insurance companies are in the business of collecting more premiums than they pay out in claims. And the way they do this is with underwriting and rate adjustment. When a property becomes a short-term rental on Airbnb, every aspect of underwriting changes.

It’s now regularly being used by guests, aka strangers to the property and these guests are unfamiliar with the property.

They may not know where the water shut-off valve is in the event of a broken water pipe, which can lead to unnecessary water damage claims.

- They may not know how to properly use the fireplace which can lead to a fire claim.

- They may not know the kitchen breaker often pops when you use the microwave and fan at the same time, which leads them to fuddle with the property’s wiring and a future fire claim.

- They may not know where the light is to use the back stars which could lead to a serious injury an liability claim.

- They may not lock the back door which could lead to a burglary or theft claim.

The List Goes On

Basically, guests do not take the same care of a property as a homeowner would. Plus, many property owners look at short-term rentals as investments, not their primary homes or residences, which leads to more insurance claims as maintenance issues are often postponed.

Why fix the roof, it’s only a rental!

When you add all this up, you get significantly more insurance claims at short-term rental properties than you do at a primary home or residence, therefore, insurance companies need to charge more in premiums to cover these claims. Or, they can and will just deny claims coverage.

Airbnb’s AirCover insurance department knows all of the above and that’s why the #3 FAQ is basically “We Recommend You Call Your Insurance Company”.

Note: Since the above lawsuit, many U.S. insurers have adopted a “home-sharing endorsement” to avoid this type of litigation, but buyers beware as they are inexpensive, only applicable to primary residences, limited in scope, and provide minimal additional coverage. What you want is a comprehensive insurance policy to fully replace your current homeowner’s insurance.

Is Airbnb’s AirCover Protection Actually Insurance?

The answer is yes and no.

All Airbnb’s AirCover protection has done is simply rebrand the longstanding Host Protection (liability protection) as ‘Host Liability Insurance’ and the Host Guarantee (property protection) as ‘Host Damage Protection’. Now it’s under one roof called ‘AirCover’, with the addition of a few coverages.

Since property damage is much more frequent, let’s deep dive into the updated AirCover Host Damage Protection first, and as seen below the answer is ‘no’, it’s not actually insurance.

This ‘not insurance’ item is important because insurance contracts offer both parties, the insurer and the insured, rights. An example of a right for the insured would be the right to a public insurance adjuster should there be a dispute. The reason every state in the union has an independent insurance commissioner is not to protect the insurer, it’s to protect the insured.

Insurance contracts are long, and confusing, and the insured needs protection from frivolous insurers

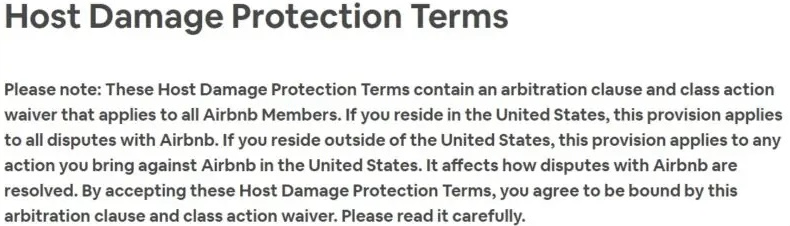

Furthermore, by agreeing to AirCover or the ‘Host Damage Protection’ portion, Hosts are agreeing to a Class Action Waiver, meaning there is virtually no recourse for a Class Action Lawsuit if Airbnb denies property damage protection to its Hosts. This is such an important point that it’s the first paragraph on the AirCover Host Damage Protection page, as seen below.

When it’s in the header, there is no argument that it was buried in the fine print

Airbnb’s AirCover Host Damage Protection wants you to be fully aware there will be no class action against them! This seems a bit off-brand and harsh in reality. Why is Airbnb so afraid of its Hosts, and in particular a class action lawsuit?

Will Airbnb’s AirCover Protection be There When You Need Property Coverage?

Since the AirCover Host Damage Protection is simply a rebrand of the Airbnb Host Guarantee we do have some history to look at. The most high-profile case we can find is from a Host in California who had a $1,800,000 fire loss.

House Fire Prompts $1,000,000 Dispute with Airbnb Then, a deeper look reveals some pretty terrible reviews:

Trustpilot : 8,247 Reviews, 1.4/5

“All hosts pay attention; this garbage bucket shop of a company claims to have insurance but trust me, from my personal experience, you are NOT insured, and if a guest makes damage to your property, they will just respond, unfortunately, your request has been denied.”

Better Business Bureau: 5,996 Complaints, 1.07/5

“AirBnB touts they provide a *************** *********** Protection, but when there is damage like a broken floor tile, doors severely scratched up, floors with deep gouges in them, they say it’s considered Normal Wear and Tear and not covered. I’m not sure in what World these damages would be considered Normal.”

Consumer Affairs: 2,571 Reviews, 3.6/5

“The last guest that I had almost destroyed my property. Damage to my artwork. Dirt and disgusting stuff were everywhere. Broken plates, cups and a big window of a French door which took me 4 days to replace. Party every night till dawn, disturbed the neighbors, and Airbnb did not take any responsibility. Shame on them.”

Airbnb Community Thread : 195+ Responses

“The story could be mine exactly AirBnb has no interest in anything but their own bottom line. Get your own insurance!!!!!”

Reddit Thread : 75+ Responses

“Airbnb Host Guarantee is completely unreliable and gives a false sense of security.”

AirHostForum Thread : 20+ Responses

“Airbnb Host Guarantee is USELESS”

AirbnbHell Threads : 5+ Threads

“Airbnb Host Guarantee Scam: No Payment for Damages.”

There is some evidence of Airbnb paying out for damage, but it’s pretty hard to ignore all these negative comments. The best approach is to rely on homeowner’s insurance and at best, think of Airbnb AirCover protection as a back-up.

Now That We’ve Discussed Property Protection, Let’s Examine the Airbnb AirCover Liability Insurance

If you recall, Airbnb AirCover is broken into two parts, property protection which is not insurance, and liability insurance, which is. The new liability insurance part of AirCover is a rebrand of the former Host Protection program, which also offered $1,000,000 in liability insurance.

Another big concern is the fact we can’t find a single review online in reference to the $1,000,000 in liability insurance coverage. However, we did find a disturbing news report from Bloomberg. Airbnb Is Spending Millions of Dollars to Make Nightmares Go Away

Regardless of whether Airbnb’s AirCover would respond to a liability claim or not, the Host is not a named insured, which means they have no policy rights. It’s solely up to Airbnb whether or not to respond to a liability claim or not on a Host’s behalf.

After seeing the Bloomberg report, it’s clear you want your own liability insurance policy with your name on it.

What is Really Going on with Airbnb’s AirCover Protection?

We can only speculate, but Airbnb is now a public company traded on the New York Stock Exchange and lost $4.6 Billion in 2020, in 2021 it started out much the same with about $1.2 Billion in losses from Q1 – Q2, but to their credit, they posted their first profitable quarter in Q3 2021.

Airbnb knows the only way to keep growing is to get new Hosts, and they must have data that shows the AirCover offering helps.

This makes sense as insurance would be considered a barrier to becoming an Airbnb Host. The problem is nothing in life is free, and from our research, it appears neither is insurance!

Like anything else, the quality of what you get is often determined by its cost. Good comprehensive insurance is not cheap, but it’s money well spent if the day ever comes when you have to use it!

Please note that the snapshots and review links included here were taken from Airbnb when the blog was written on November 19, 2021. Airbnb updates policies and content frequently, specific language may have changed.