Commercial Insurance vs. Landlord Insurance: What’s the Real Difference for Rental Properties?

A Commercial (business) insurance policy and a DP-3 Landlord policy are not the same thing—even when a Landlord policy is marketed as short-term rental coverage. The structural difference comes down to one thing: Commercial policies carry Commercial General Liability (CGL), which covers bodily injury and property damage.

Landlord policies carry premises liability, which only covers incidents that occur on the property itself. For vacation rental and home-sharing owners, that coverage gap is where most serious claims fall.

- What Is Commercial Landlord Insurance?

- The Problem With Some Short-Term Rental Policies

- Understanding Liability in Insurance

- Premises Liability vs. Commercial General Liability

- Property Coverage Gaps with Landlord Policies

- Commercial vs. Landlord Insurance for Single-Family Rentals

- Frequently Asked Questions

TL;DR: A Landlord (DP-3) policy isn’t built for short-term rentals. If a guest incident happens off-property, or an insurer decides your rental is a business, a DP-3’s premises liability won’t respond. A Commercial General Liability (CGL) policy covers both—and that’s the structural difference Proper is built on.

What Is Commercial Landlord Insurance?

If you’re a short-term rental, Airbnb, or Vrbo owner, “Commercial Landlord insurance” is a broad term that people use when they know their vacation rental is a business, but aren’t sure what coverage actually fits.

Commercial Landlord insurance—also called business insurance for rental property—is a Commercial-lines policy designed for property owners who create income from their rentals. Unlike a standard Dwelling (DP-3) policy, a Commercial Landlord policy is structured as a business insurance contract, which means it includes Commercial General Liability (CGL) rather than the more limited, premises-focused liability found in premises liability. The distinction matters most when a claim arises away from the property, or when an insurer argues that operating a short-term rental qualifies as a “business pursuit.”

For many hosts, “Commercial Landlord insurance” is shorthand for:

- “I rent my property for income”

- “I need business-level liability protection”

- “My standard Landlord or Homeowners policy probably isn’t enough”

For short-term rental owners, this term often points to a Commercial Homeowners policy—a hybrid that combines business-level liability with coverage built specifically for Airbnb and vacation rental use. Proper Insurance developed this model to bridge the gap between personal Landlord insurance and traditional Commercial policies.

The Problem With Some Short-Term Rental Policies

The most common scenario: a short-term rental owner believes they have the right coverage because their policy says ‘short-term rental’ on it. The problem is what’s underneath that label. In many cases, it’s a DP-3 Landlord policy rebranded and marketed as short-term rental coverage, sometimes with limited endorsements rather than a full structural change to coverage.

You can’t simply add a line item to a policy and call it a short-term rental insurance policy—but that’s exactly what a half-dozen carriers are doing. A Landlord (DP-3) policy isn’t built for short-term rentals. If a guest incident happens off-property, or an insurer decides your rental is a business, a DP-3’s premises liability won’t respond. A Commercial General Liability (CGL) policy covers both — and that’s the structural difference Proper is built on.

What Is a Business Pursuit or Activity Exclusion?

A business pursuits exclusion or business activity exclusion is a clause found in most DP-3 Landlord and standard Homeowners policies that eliminates liability coverage if the insured is conducting a business activity on the premises. For short-term rental owners, this exclusion creates a direct exposure: if an insurer determines that operating a vacation rental constitutes a business pursuit (which many do), your liability coverage may be reduced or excluded entirely. A Commercial General Liability policy, by design, does not carry this exclusion because it is already written as a business policy.

Uncover The Gaps In Your Policy

Learn 10 essential questions about short-term rental coverage to ask your insurance agent to understand your policy’s gaps.

"*" indicates required fields

Understanding Liability in Home-Sharing Insurance

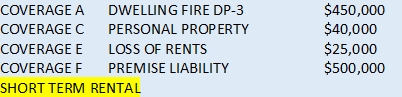

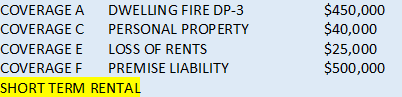

If your policy or the quote you have looks anything like the above snapshot, then there are some important things you need to know. The key terms you are looking for are Dwelling Fire-DP3, Personal Property, Loss of Rents, and most importantly, premises liability.

Liability is the most important exposure to understand when insuring a vacation rental. The premises liability language is straightforward: coverage applies for bodily injury and property damage primarily when it occurs on your property, subject to policy language and exclusions. But what about bodily injury or property damage that could occur away from the premises?

Many incidents could occur away from the premises/vacation rental for which you need liability coverage. Here are a few real examples:

- A renter brings their dog to the vacation rental during their stay, even though you don’t allow pets. The renter walks the dog off-property, and the dog bites a child. The child’s parents sue both the renter and you, the owner. This occurred away from the premises and would not be covered under premises liability.

- Note: According to the Insurance Information Institute, the average dog bite claim reached $65,450 in 2025, with U.S. insurers paying out $1.86 billion in dog-related injury claims that year—nearly double what was paid a decade ago. Learn how Proper’s Pet & Animal Liability coverage responds to incidents like this.

- You offer bicycles as an amenity to your vacation rental. A home-sharing guest rides a bicycle into town, and the chain falls off, resulting in a crash and bodily injury to the guest. The guest goes to the hospital, and their health insurance company sues you, the vacation rental/home-sharing owner, for bodily injury. This bodily injury occurred away from the premises.

- You rent your vacation rental to a family for the week of the 4th of July. The family purchases fireworks and sets them off at sundown. One of the fireworks lands on a neighboring home, and as a result, the home burns down. The neighbors’ Homeowners insurance company sues you, the vacation rental owner, for the property damage to the house. This is property damage that occurred away from the premises.

Each of these is a real-world claim scenario that premises liability would not cover, because the incident occurred away from the property.

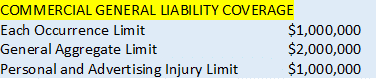

Premises Liability vs. Commercial General Liability

First, what is Commercial General Liability? Commercial General Liability (CGL) is a standard insurance policy issued to business organizations to protect them against liability claims for bodily injury and property damage arising out of premises, operations, products, and completed operations; and advertising and personal injury liability. For short-term rental owners, CGL is the coverage that matters most—and the coverage most landlord policies don’t carry. A Commercial (business) insurance policy carries Commercial General Liability instead of premises liability, and CGL extends coverage beyond the property for liability arising out of business operations, subject to policy terms, conditions, and exclusions.

Personal and Advertising Injury coverage matters for vacation rental owners for two specific reasons: invasion of privacy and slander. Believe it or not, we do see claims arising from invasion of privacy. Typically, this happens when a cleaning crew comes to the vacation rental early by mistake and invades the privacy of the guest.

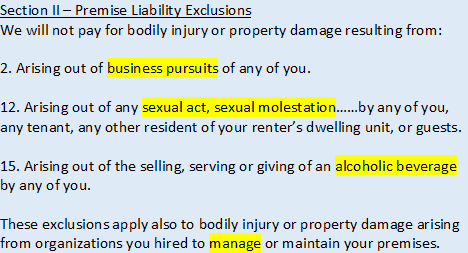

Premises liability policies carry additional exclusions worth understanding. The most significant is the business pursuits exclusion: if an insurer determines your vacation rental is a business activity—and many do—there may be significant limitations or exclusions in liability coverage at the property. In practice: if an insurer determines that operating a short-term rental constitutes a business pursuit at the time of a claim, coverage is void. A DP-3 Landlord policy is designed for traditional landlords, not businesses. If the property generates income from short-term guests, a commercial or purpose-built short-term rental policy is often more appropriate, depending on how the property is used and how the policy is written

Assuming the bodily injury did not occur off the premises, and the insurance company doesn’t deem “short-term renting” a business pursuit, there are some additional exclusions that must be noted.

Since the Proper Insurance policy is a business policy and we removed the liquor liability exclusion, all of the above are covered as well:

- Alcohol furnished by the rental

- Business pursuits

- Sexual assault/molestation

- Property Managers (automatically additionally insured)

Property Coverage Gaps with Landlord Policies

Beyond liability, a DP-3 landlord policy has structural gaps on the property side as well.

DP-3 Landlord Policy vs. Proper Insurance: Coverage Comparison

Short-term rental properties face a distinct set of risks that a standard Landlord policy was never designed to cover. The table below outlines the most significant structural differences between a DP-3 Landlord policy and the Proper Insurance policy—from liability type to property coverage to revenue protection.

| DP-3 Landlord Policy | Proper Insurance Policy | |

| Liability Type | ❌ Premises liability—on-property incidents only | ✅ Commercial General Liability—extends off-premises throughout the U.S. |

| Business Pursuits | ❌ Excluded—may void all liability coverage if STR is deemed a business | ✅ Included |

| Liquor Liability | ❌ Excluded | ✅ Included |

| Guest-Caused Damage | ⚠️ Limited or excluded | ✅ Included via Property Entrustment |

| Revenue Protection | ⚠️ Loss of Rents — fair market value, typically capped at 12 months | ✅ Loss of Business Revenue—actual loss sustained, no time limit |

| Vacancy | ❌ Not covered after 60 days unoccupied. | ✅ Included—vacancy clause removed |

| Property Valuation | ⚠️ Actual Cash Value (depreciated) | ✅ Replacement Cost—new for old |

Note: Coverage features vary by carrier. Some Landlord or hybrid policies may offer endorsements for short-term rentals, but these often differ significantly from a Commercial policy structure.

Loss of Rents: A DP-3 policy pays fair market rental value—meaning the average long-term rate for your area—capped at 12 months. For short-term rentals, which command significantly higher nightly rates, this creates a real underinsurance gap. A total loss rebuild can also take 18–24 months, making the cap a meaningful limitation on top of the rate problem.

The Proper Insurance policy carries “actual loss sustained” business income coverage with NO time limit. This is far superior to the loss of rent. When you own a business (vacation rental/home sharing), you want business insurance.

Additional Coverage Differences

- A standard DP-3 Dwelling policy does not cover vacant properties. The Proper Insurance policy removes the vacancy clause, so if the vacation rental goes more than 60 days unoccupied, it’s covered.

- Many DP-3 Dwelling policies carry “Actual Cash Value (depreciation)” in the event of a partial loss, and also ACV for contents/personal property. The Proper policy is replacement cost, “new for old,” for both buildings and contents.

- Most DP-3 Landlord policies carry a special form (all-risk) coverage form for building, but carry a broad form (limited to named perils only) on contents/personal property. The Proper Insurance policy carries special form coverage on all buildings, contents, and business income.

- Most DP-3 Landlord policies do not offer coverage for sewer and drain backups, which are very common claims. The Proper Insurance policy provides coverage for backups of sewers and drains with no sub-limit.

These are among the most significant structural differences—not an exhaustive list.

Commercial vs. Landlord Insurance for Single-Family Rentals

Owners of single-family rental homes often assume a DP-3 or Landlord policy is sufficient—especially if they only rent occasionally or seasonally. But the policy structure doesn’t change based on how often you rent. A Landlord policy is still a residential policy with premises liability and, in most cases, a business pursuits exclusion. A Commercial Homeowners policy is the appropriate structure any time the property generates rental income, regardless of whether it’s rented 30 nights a year or 300. For single-family short-term rentals in particular, the off-premises liability exposure from guests using amenities, bikes, or nearby recreation is identical to that of a larger vacation rental.

If you’re unsure whether your current policy is structured correctly for short-term rental use, Proper’s agents can walk you through your coverage in detail. Call 888-631-6680 or get a quote online.”

Frequently Asked Questions

Is Landlord insurance the same as Commercial property insurance?

No. Landlord insurance (typically a DP-3 dwelling policy) is a residential-lines product designed for long-term rental properties. Commercial property insurance is a business-lines product that includes broader liability protection — specifically Commercial General Liability — and is built around the assumption that the property is operating as a business. Short-term rental owners need a commercial policy structure, like Proper’s Commercial Homeowners policy, not a Landlord policy.

What’s the difference between Landlord liability insurance and General Liability insurance for rental properties?

Landlord liability insurance refers to the premises liability coverage included in a DP-3 policy—it only covers bodily injury or property damage that occurs on your property. General liability insurance (Commercial General Liability, or CGL) extends coverage to incidents that happen away from the premises and eliminates the business pursuits exclusion that can void coverage entirely for rental property owners.

Does a Landlord policy cover a short-term rental?

A DP-3 landlord policy is designed for long-term, traditional rentals. When rebranded or marketed as short-term rental coverage, it typically still carries premises liability (not CGL), a business pursuits exclusion, and loss-of-rents coverage capped at fair market value—all of which may be misaligned with how short-term rentals operate, depending on the policy and any endorsements added. A Commercial policy purpose-built for short-term rentals eliminates these structural gaps and truly protects short-term rentals like Airbnb, Vrbos, or book-direct properties.

What type of insurance form does Proper Insurance use?

Proper Insurance is written on a Commercial General Liability (CGL) form, not a DP-3 dwelling form. That distinction determines everything: a DP-3 Landlord carries premises liability and a business pursuits exclusion that can void your coverage the moment an insurer decides your rental is a business activity. A CGL form is already written as a business policy, so that exclusion doesn’t exist. It’s not a feature Proper added—it’s the foundation the policy is built on.